Legal & Tax Disclaimer: This article is for informational purposes only and does not constitute legal, tax, or financial advice. Tax laws change frequently. Always consult a qualified international tax attorney and a licensed tax professional in the relevant jurisdiction before making any residency or tax planning decisions. Citizens of countries with citizenship-based taxation (notably the United States and Eritrea) have additional filing obligations regardless of where they live.

Table of Contents

Most countries on earth operate a residence-based worldwide tax system: if you live there, you owe tax on every dollar, euro, or peso you earn — regardless of whether that money was made locally or on the other side of the planet. The United States goes even further with citizenship-based taxation, taxing its nationals on global income no matter where they reside.

A territorial tax system works differently. Under this model, the government only taxes income that is sourced within its own borders. Money earned outside the country — from a foreign employer, overseas clients, foreign investments, rental income from abroad — is simply not within the tax authority’s purview. You live there, but your foreign earnings are invisible to the local tax code.

For nomads, remote workers, and internationally mobile investors, this is a foundational distinction. Establishing tax residency in a territorial jurisdiction means your global income stream can remain largely untouched by local taxation, as long as it doesn’t originate from activities within that country.

Three important caveats apply before diving into the list:

1. “Territorial” is not uniform. Some countries apply a pure source-based test. Others have carve-outs for certain passive income, foreign investment gains after a period of residency, or remittance-based rules (where income only becomes taxable when physically brought into the country). The label is a starting point, not a guarantee.

2. It doesn’t mean zero tax. Territorial systems exempt foreign-source income. Income earned locally — from a local employer, a business serving local clients, local real estate — is typically taxed at standard rates. And social contributions, VAT, and other levies may still apply regardless of where your income comes from.

3. Your home country may still want its share. American citizens must file a U.S. return and report global income no matter where they live, though mechanisms like the Foreign Earned Income Exclusion (FEIE) and Foreign Tax Credits can significantly reduce actual liability. Always consider the obligations of your home country alongside those of your new tax residence.

The core question to ask about any territorial system: “What does this country’s tax authority define as locally-sourced income — and does my specific income type meet that definition?”

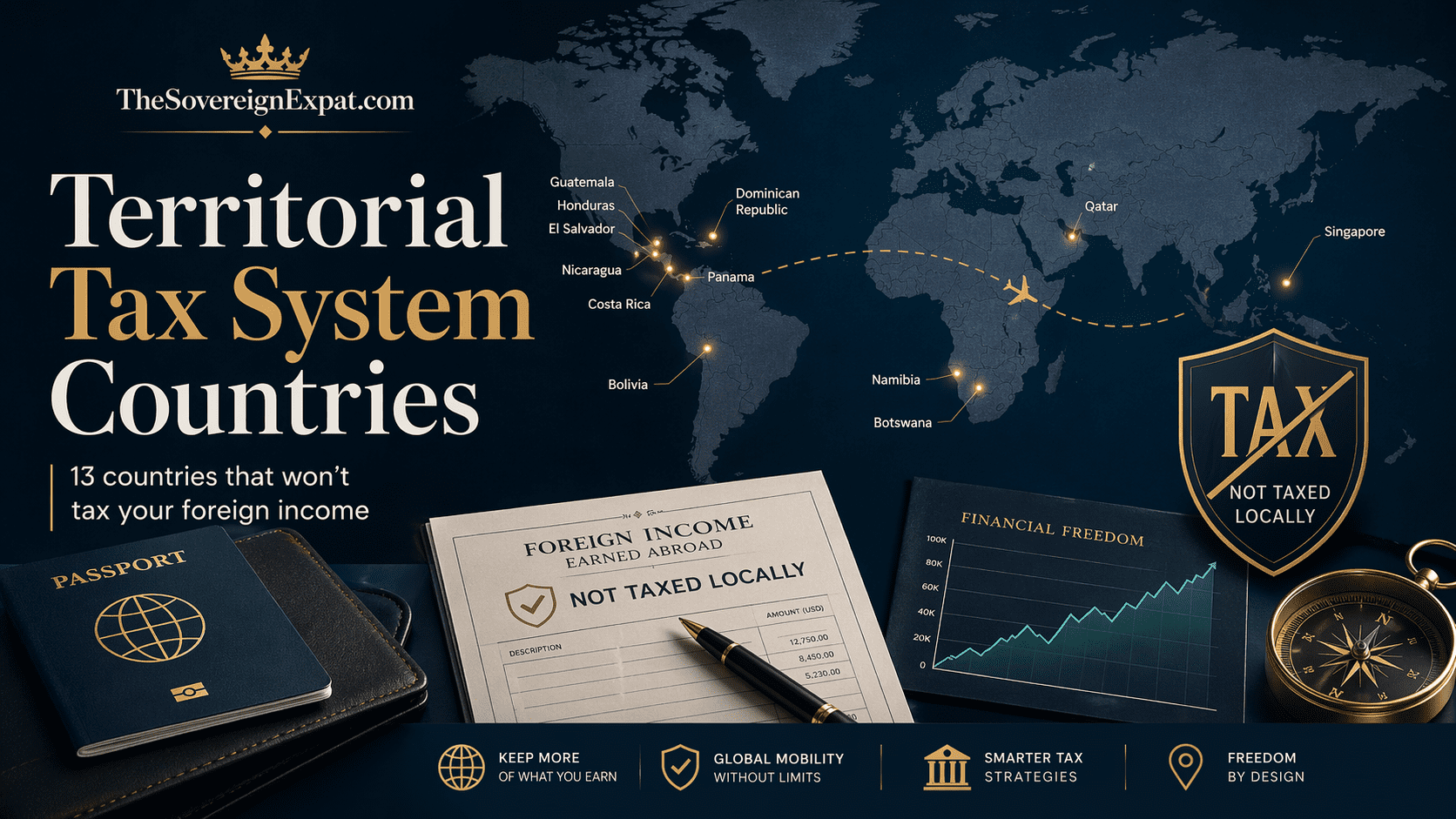

The Verified List: 13 Sovereign Countries (+ 2 Territories)

Online guides on this topic frequently recycle outdated or imprecise information, conflating zero-tax jurisdictions, remittance-basis systems, and genuine territorial models. The list below reflects the most rigorous cross-reference available as of April 2026, drawing on PwC’s Worldwide Tax Summaries, EY’s Personal Tax and Immigration Guide, IRAS (Singapore’s official tax authority), and official country-specific sources.

Based on current verified guidance, 13 sovereign nations operate a territorial or source-based system for individual resident taxpayers:

Country | System Type | Local Rate | Residency Threshold |

|---|---|---|---|

Panama | Pure Territorial | 0–25% | 183 days or residency permit |

Paraguay | Pure Territorial | 10% flat | Residency permit + DNIT registration |

Costa Rica | Pure Territorial | 0–25% | 183 days or residency permit |

Singapore | Territorial (with carve-outs) | 0–24% | 183 days in calendar year |

Nicaragua | Pure Territorial | 0–30% | 183 days or residency permit |

Honduras | Pure Territorial | 0–25% | 183 days or residency |

El Salvador | Pure Territorial | 0–30% | 183 days or residency permit |

Guatemala | Pure Territorial | 5–7% flat tiers | 183 days or residency |

Bolivia | Pure Territorial | 13% flat (RC-IVA) | 90 days in 12-month period |

Botswana | Pure Territorial | 0–25% | 183 days or residency |

Namibia | Source-Based (with deeming rules) | 0–37% | 183 days or ordinarily resident |

🇩🇴 Dominican Republic | Territorial — first 3 years only | 0–25% | 183 days or residency |

🇶🇦 Qatar | Zero Personal Income Tax | 0% (individuals) | Residency permit required |

Note: Hong Kong and Macau are major territorial jurisdictions but are not sovereign states — covered separately below.

The Core Territorial Countries — Detailed Profiles

Panama

Region: Central America · USD Economy

Tax on Foreign-Source Income: 0%. All income derived from sources outside Panama is explicitly exempt — whether remitted to Panama or not.

Tax on Local-Source Income: Progressive rates: 0% (up to $11,000) · 15% ($11,001–$50,000) · 25% (above $50,000).

Tax Residency Trigger for Foreigners: Physical presence of 183+ days in a calendar year, OR holding a valid Panamanian residency permit (even if spending fewer days in-country).

Key Residency Visas: Friendly Nations Visa (50 eligible countries) · Pensionado Visa ($1,000/mo pension) · Qualified Investor Visa ($300,000 real estate) · Digital Nomad Visa.

Capital Gains Tax: 10% on gains from Panamanian real estate and local securities. Foreign capital gains: exempt.

Other Taxes: No inheritance, gift, or wealth tax. ITBMS (VAT) of 7%.

Remote Work Nuance: If you sit in Panama and perform work for a foreign company or foreign clients, Panama’s official position is that this income is foreign-source because the economic activity is paid by an entity abroad. In practice, Panama does not pursue tax on remote salaries or freelance income paid by non-Panamanian clients. However, if you incorporate a Panamanian company and bill clients through it locally, the income becomes Panamanian-source. Maintain clear documentation that your employer or clients are outside Panama.

Official Source: Dirección General de Ingresos (DGI) — dgi.mef.gob.pa PwC Summary: taxsummaries.pwc.com/panama

Paraguay

Region: South America · Heart of the Continent

Tax on Foreign-Source Income: 0%. Paraguay’s territorial system completely exempts income earned outside the country’s borders, with no remittance conditions.

Tax on Local-Source Income: Flat 10% on employment income, business income, and dividends earned within Paraguay. No bracket complexity.

Tax Residency Trigger for Foreigners: Uniquely, Paraguay does not use a day-count test. Tax residency requires: (1) a valid residency permit, and (2) formal registration with the DNIT (tax authority). Spending 120 days establishes legal domicile for administrative purposes but is separate from tax residency.

Key Residency Visas: Simple Permanent Residency (documents + clean criminal record, no investment required) · Investment Residency ($70,000 business investment). No minimum stay required to maintain residency once granted.

Capital Gains Tax: No separate CGT. Capital gains are folded into general income and taxed at 10% if locally sourced. Foreign capital gains: exempt.

Other Taxes: No inheritance tax, gift tax, or wealth tax. IVA (VAT) of 10%. Limited tax treaty network (only 6 countries as of 2026).

Remote Work Nuance: Remote work for foreign clients is straightforwardly foreign-source income in Paraguay. There is essentially no ambiguity — the tax authority does not pursue income paid by entities outside the country. Paraguay is arguably the most straightforward territorial system in the world for digital nomads. The main caveat: Paraguay’s limited double-tax treaty network means your home country may still tax any Paraguayan-source income if you happen to earn any locally.

Official Source: Dirección Nacional de Ingresos Tributarios — dnit.gov.py PwC Summary: taxsummaries.pwc.com/paraguay

Costa Rica

Region: Central America · Pura Vida

Tax on Foreign-Source Income: 0%. Costa Rica has operated a territorial tax system since 1946. The determination is based on where the economic activity generating the income takes place, not where the money is received.

Tax on Local-Source Income: Progressive: 0% (≤₡929,000/mo) through tiers up to 25% on the highest bracket for employment income.

Tax Residency Trigger for Foreigners: 183+ days in a calendar year, or holding a valid residency permit. Legal residency typically creates a tax filing obligation.

Key Residency Visas: Rentista Visa ($3,000/mo income) · Pensionado Visa ($1,000/mo pension) · Inversionista Visa ($150,000 investment) · Digital Nomad Visa (launched 2022, $3,000/mo income).

Capital Gains Tax: 15% CGT on gains from Costa Rican assets (introduced 2019). Foreign capital gains: exempt.

Other Taxes: No inheritance or wealth tax. IVA (VAT) at 13%. Social security contributions (CCSS) apply to locally earned employment income.

Remote Work Nuance: This is a genuine grey area. The official territorial rule is clear — income from abroad is not taxable. But if a foreign national lives in Costa Rica and provides services to a foreign company, some advisors argue the work is being performed in Costa Rica, potentially creating a source nexus. In practice, Costa Rican authorities have not broadly pursued remote workers’ foreign salaries, and most practitioners interpret foreign-paid remote work as foreign-source. The Digital Nomad Visa explicitly exempts its holders from local income tax, providing the clearest statutory protection. If you are earning remotely, this is the visa to use.

Official Source: Ministerio de Hacienda — hacienda.go.cr PwC Summary: taxsummaries.pwc.com/costa-rica

Singapore

Region: Southeast Asia · City-State

Tax on Foreign-Source Income: Generally exempt for individual tax residents. Foreign-source income received in Singapore by resident individuals is exempt from tax, unless received through a Singapore partnership.

Tax on Local-Source Income: Progressive rates from 0% to 24%. No capital gains tax, no inheritance tax, no estate duty.

Tax Residency Trigger for Foreigners: 183+ days in a calendar year; OR employment straddling two calendar years totalling 183+ days; OR a work pass valid for 1+ year (subject to final IRAS review). Directors, public entertainers, and professionals have separate treatment.

Key Residency/Work Visas: Employment Pass (min. S$5,000/mo salary) · EntrePass (entrepreneurs) · ONE Pass (top talent, S$30,000/mo) · Personalised Employment Pass. No dedicated digital nomad visa as of 2026.

Capital Gains Tax: No CGT for individuals. Foreign investment gains: exempt. (Note: IRAS may characterise frequent trading as a trade, making profits taxable.)

Other Taxes: GST (VAT) at 9%. CPF (social contributions) apply only to Singaporeans and PRs, not to Employment Pass holders. No wealth or inheritance tax.

Key Exceptions to Know:

- Foreign income received through a Singapore partnership is taxable.

- If IRAS determines that the profit-generating activities of your business occurred in Singapore — even if clients are overseas — the income may be treated as Singapore-source and taxed.

- The Foreign-Source Income Exemption (FSIE) regime for companies requires economic substance tests for multinational entities receiving certain passive income.

Remote Work Nuance: An expat employed by a Singapore company is taxed on their full employment income regardless of where tasks are performed. An expat who is a Singapore tax resident but employed entirely by a foreign entity with no Singapore-based duties has a more favourable analysis. The key question is: Who employs you, and where are your duties performed?

Official Source: IRAS — iras.gov.sg/taxes/individual-income-tax

Bolivia

Region: South America

Tax on Foreign-Source Income: 0%. Bolivia taxes only income from Bolivian sources. The RC-IVA applies only to domestic income.

Tax on Local-Source Income: RC-IVA at a flat 13% on employment income from Bolivian sources, creditable against VAT paid. Corporate income tax (IUE) at 25%.

Tax Residency Trigger for Foreigners: Physical presence of 90 days within any 12-month period. This is one of the lowest thresholds in the world and means nomads on extended stays can inadvertently trigger residency.

Capital Gains Tax: Gains from Bolivian assets are taxable. Foreign capital gains: exempt.

Other Taxes: IVA (VAT) at 13%. IT (Transaction Tax) at 3% on gross income for businesses. No inheritance or wealth tax.

Note for Nomads: Bolivia’s 90-day threshold means you can become a tax resident during an extended visit even without formal residency. Track your days carefully.

Official Source: Servicio de Impuestos Nacionales — impuestos.gob.bo PwC Summary: taxsummaries.pwc.com/bolivia

El Salvador

Region: Central America · Bitcoin Legal Tender

Tax on Foreign-Source Income: 0%. Only income from Salvadoran sources is taxable for residents.

Tax on Local-Source Income: Progressive: 0% (up to $4,064/yr) · 10% · 20% · up to 30% (above ~$28,000/yr).

Tax Residency Trigger for Foreigners: 183+ days in a tax year, or holding a valid residency permit.

Key Residency Visas: Rentista Visa ($1,000/mo) · Pensionado Visa ($1,000/mo) · Inversionista Visa. El Salvador has been aggressively courting crypto entrepreneurs and investors.

Bitcoin / Crypto: As Bitcoin is legal tender, BTC transactions are not subject to capital gains tax. Foreign crypto gains from foreign exchanges are arguably exempt as foreign-source income.

Other Taxes: IVA (VAT) at 13%. No wealth tax or inheritance tax.

Official Source: Ministerio de Hacienda — mh.gob.sv PwC Summary: taxsummaries.pwc.com/el-salvador

Guatemala

Region: Central America

Tax on Foreign-Source Income: 0%. Guatemala taxes only income derived from Guatemalan economic activities.

Tax on Local-Source Income: Two regimes: (1) Simplified regime: 5% on revenues under Q30,000/quarter, 7% above; (2) General regime: 25% on net profits. Employment income: 5% (up to Q300,000) and 7% above.

Tax Residency Trigger for Foreigners: 183+ days during any 12-month period, or holding a valid residency permit.

Key Residency Visas: Residency by rentista ($1,000/mo) · Investment residency · Pensionado program. Guatemala is an underrated option with low cost of living and direct flights to the US.

Official Source: Superintendencia de Administración Tributaria — sat.gob.gt PwC Summary: taxsummaries.pwc.com/guatemala

Honduras

Region: Central America

Tax on Foreign-Source Income: 0%. PwC’s Honduras guide is explicit: residents are taxed only on Honduran-source income.

Tax on Local-Source Income: Progressive: 0% (≤L200,000) · 15% · 20% · 25% (above approx. L1,500,000).

Tax Residency Trigger for Foreigners: 183+ days during a tax year, or holding a valid residency permit.

ZEDE Note: The Próspera Special Economic Zone on Roatán had its own tax framework that was legally contested. Verify the current status of any ZEDE-specific tax rules with local counsel before relying on them.

Official Source: Servicio de Administración de Rentas — sar.gob.hn PwC Summary: taxsummaries.pwc.com/honduras

Nicaragua

Region: Central America

Tax on Foreign-Source Income: 0%. Nicaragua’s IR (Impuesto sobre la Renta) applies only to Nicaraguan-source income.

Tax on Local-Source Income: Progressive: 0% (≤C$100,000) up to 30% (above C$1,000,000).

Tax Residency Trigger for Foreigners: 183+ days in any calendar year, or holding a valid Nicaraguan residency permit. Residency permits require 6 months of annual presence to maintain.

Key Residency Visas: Rentista ($750/mo) · Pensionado ($600/mo) · Inversionista ($30,000 min.) · Resident by investment in a Nicaraguan SA.

Safety Advisory: Nicaragua’s political environment has deteriorated significantly since 2018. Several Western governments advise heightened caution. The tax system is genuinely territorial and residency is accessible, but quality of life, safety, and freedom of movement are serious concerns that must factor into any residency decision.

Official Source: Dirección General de Ingresos — dgi.hacienda.gob.ni PwC Summary: taxsummaries.pwc.com/nicaragua

Botswana

Region: Southern Africa

Tax on Foreign-Source Income: 0%. Botswana residents are taxed only on income from Botswana sources.

Tax on Local-Source Income: Progressive: 0% (≤BWP36,000/yr) · 5% · 12.5% · 18.75% · up to 25%.

Tax Residency Trigger for Foreigners: 183+ days in Botswana during a 12-month period. Ordinary residence (established domicile) also triggers full residency status.

Expat Appeal: Politically stable, well-governed, English-speaking, low corruption, diamond-backed economy. Popular with professionals in mining and development. Growing interest from location-independent workers attracted by its stability within the African context.

Official Source: Botswana Unified Revenue Service — burs.org.bw PwC Summary: taxsummaries.pwc.com/botswana

Namibia

Region: Southern Africa

Tax on Foreign-Source Income: Generally 0%, but Namibia has “deeming provisions” that can reclassify income as Namibian-source depending on where services are physically rendered or where certain assets are situated.

Tax on Local-Source Income: Progressive: 0% (≤N$50,000) through tiers up to 37% on income above N$1,500,000.

Tax Residency Trigger for Foreigners: 183+ days in Namibia during the tax year, OR being “ordinarily resident” (established home and centre of vital interests in Namibia).

Important Caveat: Namibia’s deeming rules mean that income from services physically performed inside Namibia may be treated as Namibian-source, even if the client or employer is abroad. This is more nuanced than Panama or Paraguay’s clean territorial rules. Nomads working from Namibia for foreign employers should obtain a specific written legal opinion before relying on the territorial exemption.

Official Source: Ministry of Finance Namibia — mof.gov.na PwC Summary: taxsummaries.pwc.com/namibia

Dominican Republic

Region: Caribbean

Tax on Foreign-Source Income: 0% during the first 3 years of residency. After year three, certain foreign passive investment income (dividends, interest) becomes taxable. Active employment income from abroad generally remains exempt.

Tax on Local-Source Income: Progressive: 0% (≤RD$416,220) up to 25% (above RD$867,123).

Tax Residency Trigger for Foreigners: 183+ days, or holding a valid residency permit.

Key Residency Visas: Rentista ($1,500/mo) · Pensionado ($1,500/mo) · Inversionista ($200,000 investment) · Digital Nomad Visa (requires $1,500/mo income).

Critical Note: The DR’s territorial exemption for foreign investment income expires after 3 years of residency. This makes the DR well-suited for short-to-medium-term planning, or for those whose foreign income is primarily active employment or service income (which generally remains exempt longer term). Anyone planning to stay long-term should seek current local counsel on their specific income mix.

Official Source: Dirección General de Impuestos Internos — dgii.gov.do PwC Summary: taxsummaries.pwc.com/dominican-republic

Qatar

Region: Middle East · Gulf State

Tax on Foreign-Source Income: 0%. Qatar levies no personal income tax whatsoever on individuals — on any income from any source.

Tax on Local-Source Income: 0% personal income tax. Corporate income tax of 10% applies to Qatari-source business income.

Tax Residency Trigger for Foreigners: Qatar requires a valid residency permit (iqama), typically tied to employment or investment. The Golden Visa (Residency by Investment) starts at $200,000 in real estate; $1,000,000+ may qualify for permanent residency.

Key Residency Visas: Work Residency (employer-sponsored) · Qatar Golden Visa · Long-term residency for certain professionals and retirees.

Practical Considerations: High cost of living. Kafala (sponsorship) system for employment residency. No general pathway to citizenship for most foreigners. Conservative social laws. Excellent infrastructure and personal safety.

Classification Note: Qatar is technically a zero personal income tax jurisdiction rather than a “territorial” system — the distinction is moot for individuals since no income is taxed regardless of source.

Official Source: General Tax Authority of Qatar — gta.gov.qa PwC Summary: taxsummaries.pwc.com/qatar

Notable Territories: Hong Kong & Macau

These two territories deserve prominent mention even though they are not sovereign states. Both operate robust territorial tax frameworks and are major hubs for internationally mobile professionals.

Hong Kong SAR

Tax on Foreign-Source Income: 0%. The IRD taxes only income from Hong Kong sources. If your work and your clients are entirely outside Hong Kong, the income is not taxable.

Tax on Local-Source Income: Salaries Tax: Progressive 2%–17%, or standard rate of 15% on net income (whichever is lower). Profits Tax for companies: 8.25% (on first HK$2M) and 16.5% above.

Tax Residency Trigger for Foreigners: Hong Kong does not have a formal “tax residency” concept for salaries tax — the source of the income is the determining factor, not residence per se. Work performed in HK is taxable; work entirely abroad is not. Residency is established through work visas, investment visas, or the Quality Migrant Admission Scheme.

FSIE Regime (Updated 2023): The Foreign-Source Income Exemption regime now requires multinational enterprise entities to meet economic substance tests to maintain exemptions on certain passive income types. This primarily affects large corporate groups, not individual employees or sole practitioners.

Official Source: Inland Revenue Department — ird.gov.hk

Countries That Fell Off the List: Thailand, Malaysia & Portugal

Three jurisdictions that were widely promoted as territorial or quasi-territorial tax havens have materially changed their rules in recent years. Anyone relying on older information risks a costly mistake.

Thailand — No Longer Territorial (As of January 1, 2024)

Thailand was, for decades, the archetypal expat-friendly jurisdiction for foreign income. The old rule allowed Thai tax residents to defer remittance of foreign income to the following calendar year, rendering it effectively tax-free. That loophole closed on January 1, 2024.

Under current Thai Revenue Department guidance, foreign-source income earned in tax years starting on or after January 1, 2024 is taxable when remitted to Thailand — regardless of the year of remittance. Tax residents (present 180+ days/year) who transfer money to Thailand now face progressive rates of 5–35% on those funds. Thailand is no longer a territorial system for individual residents in any meaningful sense.

Malaysia — Now Taxes Foreign-Source Income

Malaysia followed a similar path. Historically, foreign-source income was exempt. As of January 1, 2022, resident individuals became subject to tax on foreign-sourced income received in Malaysia. The official LHDN (Inland Revenue Board) guidance confirms this. Some narrow exemptions exist for certain categories, but the broad “Malaysia is territorial” shorthand that circulated for years is no longer accurate.

Portugal NHR — Closed as of Early 2025

Portugal’s Non-Habitual Resident regime was one of Europe’s most attractive non-domicile-style frameworks. It closed to new applicants at the start of 2024, with the transition period ending in early 2025. The replacement “IFICI” regime (informally called NHR 2.0) restricts eligibility to high-value-added sectors such as scientific research. Most digital nomads and general expats no longer qualify.

The lesson: Territorial tax systems are not permanent fixtures. They are policy choices that governments can — and do — reverse. Building a residency strategy around a jurisdiction requires staying current with official tax authority guidance, not relying on blog posts from 2019.

The Remote Work Grey Zone: Working in Country for Foreign Clients

This is the single most important nuance for digital nomads and remote workers — and it is frequently glossed over in popular expat content.

The core question: If I sit in Country X and perform work for Client Y who is based abroad, is that income “foreign-source” or “local-source”?

The answer varies significantly by jurisdiction.

The Pure Source Rule (Panama, Paraguay) In Panama and Paraguay, the territorial rule is applied based on where the payer is located and where the economic activity generating the payment is deemed to occur. Panama’s Fiscal Code explicitly treats income from foreign economic activity as foreign-source. In practice, authorities in both countries have consistently treated salaries and freelance income paid by foreign entities as foreign-source, even when the work is physically done in-country.

The Work-Performed Rule (Singapore, Namibia) Singapore’s IRAS looks at where employment duties are exercised. Employment income for work physically performed in Singapore is Singapore-source income — regardless of who pays you. If you are employed by a foreign company but your work is done in Singapore, that income is taxable in Singapore.

Costa Rica’s Ongoing Grey Area Costa Rica’s territorial rule is based on where the “economic activity generating the income” takes place. This creates genuine ambiguity for remote workers. The tax authority has not issued definitive guidance on remote work specifically. The Digital Nomad Visa provides explicit statutory exemption for its holders — making it the safest legal basis for foreign-paid remote workers in Costa Rica.

Practical Tax Guidance for Nomads

- Use a Digital Nomad Visa where available — it typically provides explicit statutory protection.

- In jurisdictions without DNV protection, obtain a written legal opinion from a local tax attorney confirming your income type is treated as foreign-source.

- Avoid incorporating a local company through which you bill foreign clients — that can transform foreign income into local income.

- Maintain clear documentation: foreign contracts, foreign bank accounts receiving payment, and correspondence showing the client relationship is with entities abroad.

The Watchlist: Countries Worth Watching

Georgia

Not a true territorial system, but the Individual Entrepreneur regime (1% tax on turnover up to GEL 500,000) with Small Business status effectively exempts most foreign-source income for qualifying entrepreneurs. Popular with nomads but requires careful structuring.

Uruguay

Offers a 10-year exemption on foreign passive income for new residents. After the holiday, certain foreign dividends and interest become taxable. Excellent for medium-term planning; follow updates on passive income thresholds.

Ecuador

An 11-year exemption on foreign-source income for new resident foreigners. After the period, a worldwide tax system applies. Attractive for a decade-long window but not a permanent territorial regime.

UAE

No personal income tax at all, making the territorial/worldwide distinction irrelevant for individuals. The 9% corporate tax (introduced 2023) applies to businesses. Golden Visa and Digital Nomad Visa available. The most straightforward option for high earners who can meet the cost of living.

Bahrain

No personal income tax. GCC residency available through employment or investment. Lower cost of living than the UAE with a similar tax profile.

A Note for U.S. Citizens

This entire guide assumes you can fully escape your home country’s tax reach by establishing residency in a territorial jurisdiction. For most nationalities, that is correct. But not for Americans.

The United States operates citizenship-based taxation — one of only two countries in the world to do so (the other is Eritrea). American citizens and green card holders must file a U.S. tax return and report worldwide income every year, regardless of where they live. Establishing residency in Panama, Paraguay, or Singapore does not remove the U.S. filing obligation.

That said, meaningful relief mechanisms exist:

Foreign Earned Income Exclusion (FEIE)

The Foreign Earned Income Exclusion allows qualifying Americans abroad to exclude approximately $130,000 (2025, indexed annually) of earned income from U.S. taxation, if they meet the Bona Fide Residence Test or the Physical Presence Test.

Foreign Tax Credit (FTC)

The Foreign Tax Credit is a dollar-for-dollar credit for foreign taxes paid. In purely territorial countries where little or no local tax is paid, the FTC may not fully offset U.S. liability — particularly on passive income.

Foreign Housing Exclusion

The Foreign Housing Exclusion is an additional exclusion for qualifying housing costs paid from foreign earned income.

For Americans, the best territorial tax jurisdictions are those where the combination of FEIE + FTC brings U.S. liability close to zero. This requires professional U.S. expat tax counsel — not just local tax advice. Work with a firm that specialises in U.S. expatriate taxation alongside local advisors in your target country.

How to Choose the Right Territorial Base

For the pure-tax-efficiency nomad who wants simplicity: Paraguay. No day-count requirement, 0% on all foreign income, 10% flat on local income, no inheritance or wealth tax, and one of the world’s fastest and cheapest formal residency processes.

For the lifestyle-driven expat in the Americas: Panama. The best blend of tax efficiency, infrastructure, English-language access, USD economy, and quality of life. Direct flights worldwide, strong banking, and the Friendly Nations Visa covers 50 nationalities.

For a Southeast Asia base: Singapore. The gold standard for legal and institutional quality, banking infrastructure, and regional connectivity. Higher cost of living and stricter work visa requirements, but unmatched in terms of rule of law and business environment.

For the high-income professional who wants zero tax, period: The UAE or Qatar. Zero personal income tax on any income from any source. Gulf residency has practical constraints — sponsorship, cost of living, social restrictions — but for pure tax efficiency, nothing is cleaner.

For the European who wants to stay close to home: True territorial systems inside the EU or EEA are essentially nonexistent for individuals. The closest options are Georgia (Individual Entrepreneur regime), Andorra (flat 10%, some exemptions), or Malta (remittance basis for non-domiciled residents). All require careful individual analysis.

This article will be updated as tax laws evolve. Always verify current rules with the official tax authority of the relevant country and consult a qualified cross-border tax professional before making any residency decisions.

Sources: PwC Worldwide Tax Summaries · EY Worldwide Personal Tax and Immigration Guide 2025–26 · IRAS Singapore (iras.gov.sg) · Tax Haven Directory (taxhavendirectory.com) · DGI Panama · DNIT Paraguay · Ministerio de Hacienda Costa Rica · Ministerio de Hacienda El Salvador · SAT Guatemala · SAR Honduras · DGI Nicaragua · BURS Botswana · GTA Qatar · IRD Hong Kong · Wikipedia: International Taxation